Public transportation is a basic service, but for those without a bank account, even buying a ticket can become a daily obstacle.

That’s the silent barrier faced by millions around the world—people who rely on public transport but remain excluded from modern payment systems. As transit networks phase out cash and push digital payments, those without banking access are left behind. It’s not because they can’t pay, but because the system isn’t built for them.

That’s where smart transit cards, powered by closed-loop auto fare collection systems, step in. These cards offer an accessible, secure, and cash-friendly way for the unbanked to move freely through a city.

But how?

That’s exactly what you’re going to find out in this blog.

Here’s what it covers:

- How smart transit cards can drive financial inclusion in public transport

- The key features that make them work for underserved communities

- Why transit authorities like yours should prioritize inclusive fare infrastructure

Let’s get to the basics first.

What are smart transit cards?

Smart transit cards are contactless, reloadable payment cards used to pay for travel within a transit system.

Unlike open-loop payments that rely on cards issued by banks, smart transit cards are typically part of a closed-loop auto fare collection system.

That simply means the card is issued and managed entirely by transit operators like you. There are no banks or other third-party financial institutions involved. And these cards can only be used to pay for transit services.

Passengers can top up the card at designated locations and use it across buses, metros, trains, ferries, etc.. The funds are stored directly on the card or within a linked account inside the AFC system. It’s fast, secure, and doesn’t require an internet connection or mobile device to work.

When traditional payments leave people behind

Statistics from the World Bank state that globally, over 1.4 billion people remain unbanked. That means almost one and a half billion people don’t have access to even basic financial services.

In many cities, transit systems are moving toward cashless payments and app-based ticketing. That’s a sign of progress, surely. But it often, unintentionally, excludes this segment of the population.

And that’s a problem. If your transit ticketing system only accepts bank cards or digital wallets, you’re assuming every rider has access to formal banking and technology. That’s alright for most people, especially in big cities.

But many low-income workers, migrants, and people with low education may feel left out or neglected.

They’re left to rely on limited cash ticket options that are less convenient and harder to find. Plus, they are becoming obsolete gradually.

That’s not just a passenger problem; it’s a service design problem. But it doesn’t have to be like this.

And that brings us to…

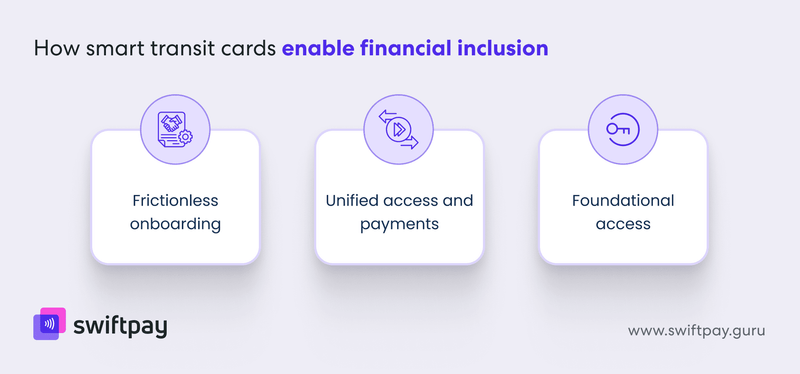

How smart transit cards enable financial inclusion

Closed-loop smart cards offer a practical middle ground between cash and digital banking. They’re easy to access, easy to use, and don’t require personal data or financial history.

Here’s how smart transit cards in a closed-loop AFC system help build a more inclusive fare environment:

Frictionless onboarding

Many public transport systems unintentionally exclude people by requiring digital wallets, bank-issued cards, or mobile apps. Closed-loop prepaid cards cut through this friction. They allow anyone—even those without a bank account—to access and use public transit through simple, prepaid top-ups.

Passengers don’t need to go through complex account setups or digital platforms. This lowers the barrier to entry for the most underserved and unbanked populations and makes the system immediately usable.

Unified access and payments

One of the most overlooked barriers for unbanked users is system fragmentation, which means they have to buy separate tickets or passes for different transit services.

Smart transit cards make it possible to pay for all transit services through a single card. Whether it’s a metro, bus, ferry, or tram, passengers use one card, one balance, and one experience. This consistency reduces confusion and cost for users. It also simplifies operations for transit authorities like you.

Foundational access

For many people, smart cards are their first exposure to a cashless, structured financial tool. Unlike mobile wallets or bank accounts, there’s no risk of debt, overdraft, or hidden fees. The simple act of loading value and tracking fare deductions introduces users to money management in a safe and controlled environment.

Over time, this familiarity can help build trust in formal systems, laying the groundwork for broader financial inclusion.

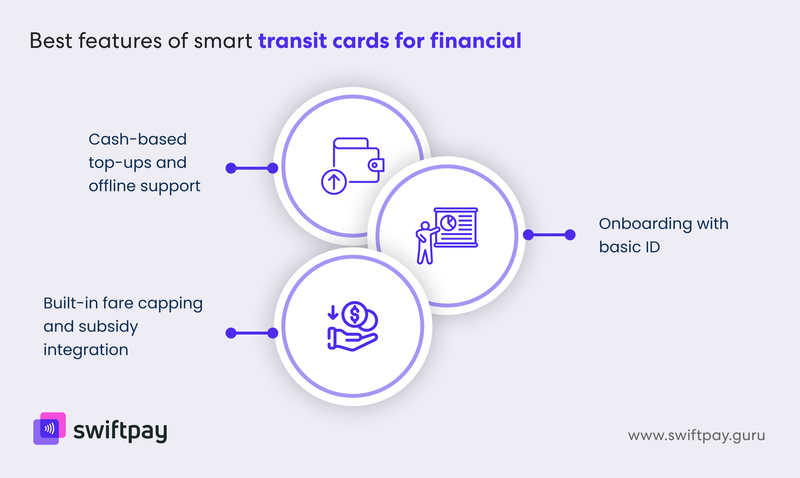

Top smart transit card features that support financial inclusion

Smart transit cards in closed-loop AFC systems are designed to work for everyone. But a few features stand out when it comes to serving unbanked or underserved populations:

Cash-based top-ups and offline support

Not every rider has a bank app, but nearly everyone can access cash. So, smart transit cards allow cash top-ups through authorized station counters, vending kiosks, or agents.

As funds are stored locally (on the card), users don’t need to rely on mobile networks or online systems to validate their balance.

This ensures the system stays accessible, regardless of a passenger’s financial or digital situation.

Onboarding with basic ID

Smart transit cards don’t require a formal bank account or credit history. People can acquire a card through transit operators, often with minimal documentation or a basic ID.

This makes it easier for people without address proof, formal employment, or government-issued ID to participate.

While some level of user verification may be required by transit authorities for card issuance or recharge, it’s entirely independent of the banking system.

People aren’t screened based on credit risk or financial background; they’re simply passengers. And the system is built to serve them on those terms.

Built-in fare capping and subsidy integration

Closed-loop AFC systems can incorporate fare capping rules to ensure that riders never pay more than a daily or monthly limit, regardless of how many trips they take.

The system can also integrate subsidy programs for students, senior citizens, or low-income groups.

These features make transit not just accessible, but genuinely affordable.

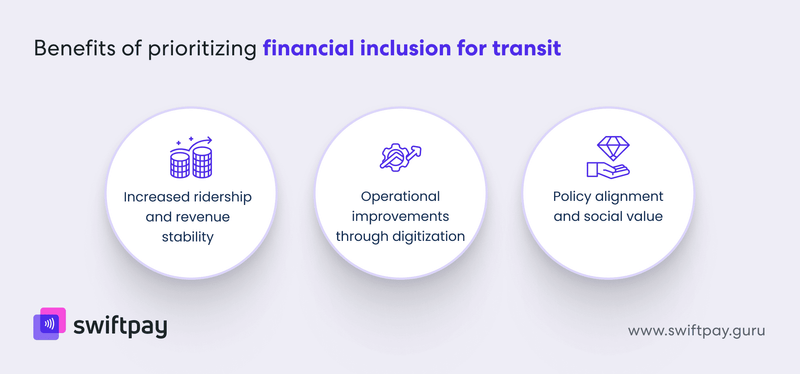

Why public transit operators should prioritize financial inclusion

When public transit leaves segments of the population behind, then it’s a social issue. But you also have to realize that it’s a business limitation as well, because you, as a transit authority, are missing out on revenue.

Financial inclusion expands both access and impact. Here’s why it matters:

Increased ridership and revenue stability

By enabling access for unbanked and low-income populations, operators expand their user base. These groups rely heavily on public transport, and giving them a secure, consistent payment method encourages more frequent usage and long-term retention.

Operational improvements through digitization

Reducing reliance on cash reduces collection overhead, manual reconciliation, and fraud risks. Inclusive systems that work across all demographics bring more users into digital fare collection, which benefits operations and planning.

Policy alignment and social value

Transit operators like you today are expected to support broader social goals—accessibility, sustainability, and equity. Inclusive fare systems aren’t just good governance; they help cities meet national goals around financial access, urban mobility, and digital public infrastructure.

Read more: Closed Loop vs Open Loop Auto Fare Collection: What Transit Operators Need to Know

Closed-loop AFC: The backbone of inclusive transit

The benefits of smart transit cards depend on the strength of the system behind them. A closed-loop auto fare collection system gives operators like you full control over the entire fare lifecycle—from issuing cards to tracking usage, setting rules, and managing funds.

More importantly, it gives you the flexibility to design inclusive programs:

- Support for multiple recharge channels (online, offline, kiosk)

- Real-time validation and tap-in/tap-out functionality

- Data insights to improve service planning and policy targeting

Hence, with a closed-loop AFC system in place, cities can innovate confidently, knowing they have a reliable foundation to serve every rider, regardless of their banking status.

Conclusion: Inclusion starts with infrastructure

A transit system is only as strong as its ability to serve everyone. And smart transit cards—when backed by a closed-loop AFC solution—are one of the few tools that make equity scalable.

They take something complex and make it easy. They meet people where they are, without expecting a bank account, credit score, or smartphone in return.

But inclusion doesn’t happen by default. It requires the right infrastructure, the right priorities, and the right partners.

At SwiftPay, we build closed-loop auto fare collection systems designed with inclusion at their core. Whether you're expanding metro coverage, digitizing your fare ecosystem, or aiming to serve unbanked populations better, our technology is built to help you get there—securely, efficiently, and equitably.

If you're building a transit future that works for everyone, we’d love to be part of it.